The IRPH in mortgages has been a subject of discussion and uncertainty among millions of Spanish families. Unlike the popular Euribor, this index has been the cause of numerous legal disputes.

At Domoblock, we have set out to write this article to delve into the complexity of the IRPH. We will examine everything from its operation to its current legal status and the real impact it has on your mortgage.

The acronym IRPH in mortgages stands for: Mortgage Loan Reference Index. It is an official indicator that some banking entities use to reference variable-rate mortgages in Spain.

This reference is calculated based on the average interest rate of mortgages offered by the banking entities themselves. This particularity has been the main reason for criticism and controversy.

You might also be interested in: fixed, variable mortgage or mixed.

In the past, the IRPH in mortgages came in various forms. Over time, regulations evolved, and the number of active indices was reduced. We will break down the three types of IRPH; it's worth noting that only one of them is still active today.

The IRPH for savings banks was a mortgage index calculated using the average interest rates of mortgages from former savings banks. Published monthly by the Bank of Spain, it ceased to be used in 2013 as part of the banking system's evolution.

It operated similarly to the previous one, but was based on the average interest rates of mortgage loans granted by banks. The Bank of Spain also published its value monthly.

Like the previous one, it ceased to be published in 2013 as part of a reform of reference indices.

It is the only IRPH index that remains fully in force and continues to be officially published. It remains valid because the Bank of Spain considered it suitable to replace the previous two in contracts that referenced them.

Order EHA/2899/2011 forced many entities to replace the discontinued indices with the current one. However, in some cases, they were unilaterally replaced by other indices without due transparency.

The IRPH mechanism in mortgages works like any other variable-rate mortgage: the installment is recalculated periodically by adding the index value and a differential.

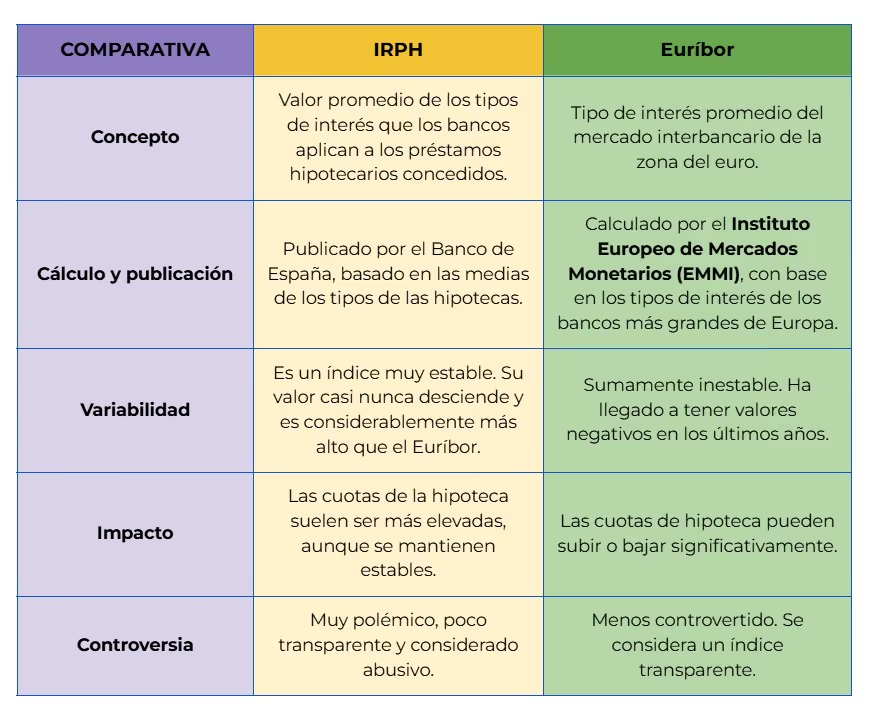

Unlike the volatile Euribor mortgage, the IRPH is a more stable but historically higher index. This stability results in higher installments for the consumer throughout the loan term.

Although both are reference indices for variable-rate mortgage loans, their characteristics and behavior are very different. In the following comparison table, we summarize the differences.

Understanding the above differences is a starting point for understanding why the IRPH has been so controversial.

The first thing you should do is gather and organize your loan documentation. Then, to find out if your mortgage is referenced to the IRPH in mortgages, you can follow these recommendations.

Carefully review your mortgage deed. Look for the clause that refers to the variable interest rate. If you find any mention of IRPH, you will know that your mortgage is linked to this index.

If for any reason you do not have your mortgage documentation, contact your bank and request a detailed statement. It should show the index used to calculate your installments.

Consult a mortgage law professional. These specialists are familiar with legal jargon and banking documents. Therefore, they are the right people to analyze your mortgage deed and confirm whether your loan has IRPH or another index.

The value of the IRPH in mortgages is published monthly by the Bank of Spain in the Official State Gazette (BOE). To calculate your installment, you must add the IRPH value plus the differential agreed upon in your contract.

Then, you must apply that percentage to your outstanding mortgage capital. For example, if the IRPH is 1.986% and your differential is 0.25%, the applicable interest will be 2.236% (1.986% + 0.25%).

Yes, it is possible to claim the abusive nature of IRPH in mortgages, even if your loan has already been canceled. The deadline for initiating legal action does not begin when the mortgage is signed or paid, but when the consumer becomes aware that the clause is abusive.

Spanish Justice, following the guidelines of the Court of Justice of the European Union (CJEU), will analyze whether the bank complied with the "double transparency control."

It is vital that the bank provides you with the information clearly and precisely. If this was not the case and you were not warned about the nature of IRPH, it is likely that the clause will be considered abusive.

Like any reference index, IRPH has two sides. Although it has a bad reputation, it offers some characteristics that could be considered an advantage, but these are overshadowed by the economic disadvantages it entails.

The main advantage of the IRPH, its stability, is outweighed by the disadvantage of its high cost. It's crucial to understand both sides to comprehend how this index affects your finances.

The legal status of the IRPH remains complex. The Court of Justice of the European Union (CJEU) requires Spanish judges to analyze the transparency of the clause, but has not declared it abusive by default. Therefore, each case must be evaluated individually.

Generally, lawyers work on a percentage of the amount recovered.

The IRPH value is updated monthly. Consult the Official State Gazette (BOE) or authorized websites.

Contact a specialist to analyze your case and guide you through the negotiation or legal claim process.

The mortgage deed, receipts for paid installments, and any other documentation related to the loan.

Current jurisprudence does not define a clear statute of limitations for abusive clauses.

The real estate sector has become accessible to everyone. With Domoblock, a platform for real estate investment, you can invest in tokenized properties starting from €200, accessing a transforming market with the security of blockchain technology and real estate crowdfunding.

Each project of flipping house and flipping building offers returns exceeding 10% and capital recovery in 8 to 12 months. Domoblock makes real estate investment agile and efficient for any type of investor.

Domoblock has various real estate investment projects in real estate investment in Madrid, real estate investment in Alicante, real estate investment in Zaragoza and real estate investment in Valencia. Check them out!

The IRPH mortgage index marked a milestone in the Spanish mortgage market. Although it is rarely used now, thousands of families continue to be affected. If your mortgage has this index, it is crucial to seek legal advice to protect your finances. At Domoblock, we can help you, contact us!

.png)

Calera, 3

Funded

100%

598.506,15 €

Target

598.506,15 €

.png)

.png)

.png)

.png)

.avif)

.avif)